In 1905, the provincial government of Sichuan began raising money for a railway. The line was to run 1,238 kilometres from Chengdu to Wuhan — a serious infrastructure project, locally conceived and locally funded. To pay for it, the government levied a 3% tax on landowners’ harvests and, in an arrangement unusual enough to be worth noting, issued share certificates in return. By 1911, the Sichuan-Hankou Railway Company had collected nearly 12 million taels of silver. Around 77% came from tax levies on farmers and landowners, the rest from public subscriptions. A substantial portion of Sichuan’s gentry and merchant class had, in one way or another, become shareholders. They had money in this railway. They cared about it.

Then the central government took it away from them.

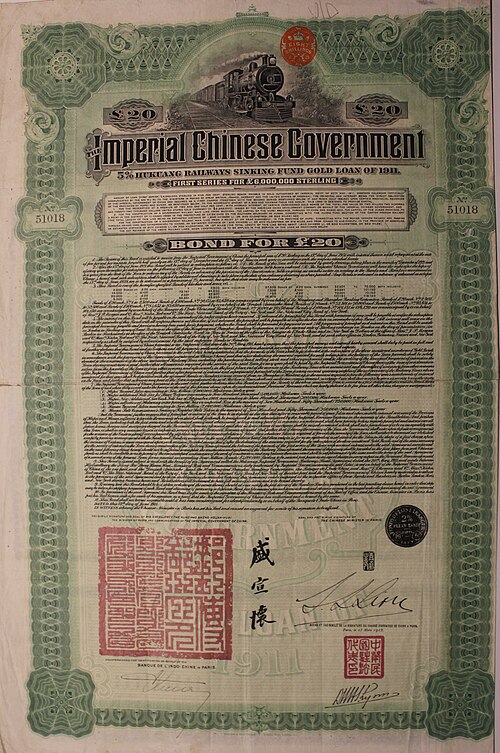

On 9 May 1911, Sheng Xuanhuai, the Qing’s Minister of Posts and Communications, announced the nationalisation of all locally controlled railway projects. Eleven days later, he signed a loan agreement with the China Consortium — a cartel of British, French, German, and American banks — pledging the operating rights to the Sichuan-Hankou and Hankou-Guangdong lines in exchange for a £6 million loan, repayable through customs duties and salt taxes. The shareholders would receive compensation: government bonds, at terms that amounted to considerably less than what Sichuan investors had put in. Sichuan was offered a worse rate than any other province.

The Qing court did not engineer this situation so much as was forced into it by previous events. The Treaty of Shimonoseki in 1895 had imposed a reparation of 200 million taels after Japan’s defeat of China. The Boxer Protocol of 1901 added another 450 million, payable over 39 years with interest. That is 650 million taels in war reparations across a single decade, from a treasury that was already stretched. The empire was broke in the structural sense — not a bad year but a permanent condition — and the only way forward was more borrowing. The Western banks were well aware of this.

The Consortium itself had been several years in the making. The British and French had been angling for railway concessions in central China since 1904, when HSBC, Jardine Matheson’s trading arm, the Pekin Syndicate, and the Banque de l’Indochine assembled a joint vehicle called Chinese Central Railways Ltd., explicitly designed to finance the lines they were now being asked to fund. Germany was brought into the arrangement not out of generosity but because a Chinese official, Zhang Zhidong, had played the Europeans against each other to secure better terms — which prompted Britain and France to include Germany rather than let it compete. A formal three-power agreement was concluded in Beijing on 6 June 1909.

The United States arrived last and most reluctantly. American bankers had shown little enthusiasm for Chinese business. Then the Taft administration decided it wanted in. Taft’s “Dollar Diplomacy” doctrine held that the export of American capital was an instrument of national power, and a China consortium without American banks was a piece of foreign influence Washington was not willing to concede. The government strong-armed its own financial institutions into a transaction they had not sought. After protracted negotiations, the four-power agreement was signed in Paris on 23 May 1910, at the head office of the Banque de l’Indochine. J.P. Morgan & Co., Kuhn, Loeb & Co., and National City Bank’s international vehicle joined the arrangement. The bankers were in China not because they saw a compelling opportunity. They were in China because their government told them to be.

The conditions attached to the loans were what made them politically impossible to absorb. British diplomat John Jordan — initially sceptical of the consortium model — designed a scheme to control Chinese government expenditure as part of the loan terms, to be overseen by the foreign commissioners of the Chinese Maritime Customs Service. The Chinese government could have the money, in other words, but foreigners would supervise how it was spent. For an empire that had already been forced to cede Hong Kong, open its ports on foreign terms, and collect customs duties under foreign supervision — that had been on the losing end of unequal treaties for seventy years — this was not a technical requirement. It was the same lesson, again. China could not be trusted to govern itself.

The Sichuan shareholders grasped this before the diplomats had finished writing the terms. The Railway Protection League, formed on 17 June 1911, organised strikes, boycotts, and mass assemblies. On 11 - 13 August, more than 10,000 protesters gathered in Chengdu. They were not simply angry about a bad financial deal, though the deal was bad. They were angry because the railway had been theirs — locally funded, locally owned, a community project converted by government decree into a debt instrument payable to foreign banks. The Sichuan gentry did not separate this transaction from the larger pattern of humiliation. They were not wrong to connect them.

On 7 September, Governor-General Zhao Erfeng had the protest leaders arrested. The crowd that marched to demand their release was met with troops. Thirty-two people were killed in Chengdu in what became known as the Bloody Chengdu Incident. Underground anti-Qing groups — the Tongmenghui, the Gelaohui — moved from the margins to open confrontation. To put down the spreading uprising in Sichuan, the court diverted New Army units from the neighbouring province of Hubei. Those were the same units that revolutionary cells in Wuhan had been counting on. On 10 October 1911 — the date China still marks as National Day — the Wuchang Uprising began: a military mutiny in Hubei, triggered ahead of schedule after a bomb-making accident threatened to expose the conspirators. It spread. Provincial governments defected. Within weeks, the Qing had lost control of southern and central China. On 12 February 1912, a six-year-old boy signed the abdication edict in his name, and two millennia of imperial rule ended.

The Consortium did not stop lending when the dynasty fell. The new republic needed money too — more desperately, if anything. Yuan Shikai, who had manoeuvred himself from general to president in the chaos of the transition, turned to the consortium almost immediately. In April 1913, the Reorganisation Loan of £25 million was signed at the HSBC building in the Beijing Legation Quarter. Sun Yat-sen denounced it publicly the day before. The loan gave Yuan the resources to defeat the parliamentary opposition that might have constrained him, enabling what Chinese historians call the Second Revolution’s failure. The consortium was not merely present at the fall of the Qing. It helped determine what came after.

As for the bonds: worthless. The railway they were issued to finance — the original Sichuan-Hankou line — was never built; the revolution made construction impossible, and the terrain made it expensive. A partial substitute, the Chengdu-Chongqing Railway, opened in 1955 under communist rule, along a completely different route. In 1983, more than 300 American investors attempted to force the People’s Republic to honour the original Hukuang bonds. They failed. The long-planned section of the original route finally opened in 2012, as part of China’s high-speed rail network — a century late, built without a foreign consortium, and entirely at China’s own expense.

The arc here is not subtle. A group of Western banks, operating under government direction, extracted harsh lending conditions from a state too indebted to refuse them. Those conditions helped ignite a revolution. The investors lost their money. The ruling dynasty ended. And China, having spent much of the twentieth century as a debtor nation under foreign financial oversight, is now the world’s largest bilateral creditor. Its Belt and Road Initiative has extended loans across more than 150 countries. The terms it attaches to those loans have been criticised, with some justice, for their opacity and the leverage they create over smaller borrowers. But no foreign commissioner audits Chinese customs receipts. No foreign diplomat designs the conditions under which China spends its own money.

The first consortium’s bankers went home empty-handed. China went through a rough period, eventually recovered and now is one of the largest powers in the world.